THE EVOLVING LANDSCAPE OF WEALTH MANAGEMENT AND THE WEALTH MANAGER

“When money realizes that it is in good hands, it wants to stay and multiply in those hands.”

—Idowu Koyenikan, Wealth for All: Living a Life of Success at the Edge of Your Ability

Wealth management is popularly defined as a high-level professional service that charges one set fee for financial and investment advice, accounting and tax services, retirement planning, and legal or estate planning. It’s become more than just advice or consulting; it’s an integral aspect of managing the entire financial lifespan—whether to address present or future needs and imperatives.

In the global finance market, wealth management is not a new concept. Widely believed to be close to 100 years old, the term was reportedly popularized by established companies such as Goldman Sachs or Morgan Stanley to segregate their regular financial customers from the wealthy private ones. Over time, providing wealth management services and expertise became popular with banks and financial services. However, the global financial crisis of 2009 changed the dynamics of the industry. It became evident that individuals and corporates needed far more education and awareness about managing their wealth.

The financial markets bounced back after the 2009 global financial crisis. However, there was a sea change in the way the markets operated and several key trends began to emerge. Three trends stood out significantly: the evolution of digital technology, a renewed and stringent focus on regulations, and the subsequent changes in the customer behaviors and demands. While most of the banks that survived the crisis benefitted from the improved market performance, their business priorities underwent significant changes, with most of them altering their business models to incorporate lessons learned from past mistakes.

This short sojourn into the history of wealth management only proves that as a vital service in financial management, the sector has evolved and the role of the wealth manager is more critical than ever before. The financial crisis gave these wealth managers/advisors the opportunity to strengthen their credibility with their customer. They became the caretakers and well-wishers of their customer’s financial lives and put their customer’s interests ahead of their own.

THE CHALLENGES OF BEING AN EFFECTIVE WEALTH MANAGER

The global wealth management industry bounced back after the economic crisis. Now, with the significant growth in the emerging markets, there is a definite increase in the number of high net worth individuals (HNWI) as well as their total wealth. The products and services demanded by HNWIs are much more complex than those offered under normal banking services. However, the growth in the wealth management business is not without its challenges. Depending on the way wealth managers address these challenges, customers can either expect windfall gains or crippling losses.

Some of the main challenges faced by wealth managers today include: adapting to the latest technological advancements, staying relevant to the next generation of investors, and finding ways to sync AI into the client-service process and investment decision-making.

■ Disruptive, yet transformation impact of digital technologies

Much like other industries, technology is realigning the business of wealth management today. While the business model is changing, technology also offers tools that improves customer communication, software that predicts better results, and analytics that forecasts with better accuracy and efficiency. With these advancements, there is a vast amount of data in the hands of the wealth manager. Advanced analytics and cognitive tools, and machine learning can be leveraged to extract maximum value from this big data. Specifically, the use of analytics tools is imperative to go beyond extracting just customer or market segmentation. These tools can specifically be used to monitor and predict customer behavior, and analyze the market as well. The challenge before wealth managers is creating this digital infrastructure and driving an improved business model for their customer benefit. managers is creating this digital infrastructure and driving an improved business model for their customer benefit.

■ Evolving customer demands to meet new advancements

Smartphones—the seemingly simple yet essential element of our everyday lives—are changing the business environment. The demand is here and now, with customers having access to a variety of products and services at their fingertips. Another important advancement is the use of mobile technologies. With the changing demographics, the younger clientele for wealth management is tech-savvy. It is estimated that around 30 percent of customers across all age groups are open to engaging remotely with an advisor who does not live near them.

The need for personalization and improved customer communication, coupled with competitive interest rates, is bringing higher expectations to wealth managers.

Currently, the focus is shifting away from HNWIs and with broad-based software and technologies available, advisors need to focus on different market segments. This just means that customers today have a better and holistic perspective of their financial needs and expect wealth managers to provide an improved and involved customer experience.

■ Reimagining the business model

Today’s wealth management companies must rise to the aforementioned challenges. Reimagining strategic business models and realigning long-term, operational strategies are critical goals. Leveraging technology platforms and software to diagnose, analyze, and predict future patterns will ensure better results for customers. Social media and mobile technologies serve to improve communications in real time. Also, wealth management companies are now looking at enhanced reporting tools to improve the overall advisory process.

THE WEALTH MANAGEMENT CONUNDRUM: HOW CAN WEALTH MANAGEMENT FIRMS AND WEALTH MANAGERS BE MORE EFFECTIVE?

The wealth management industry has evolved and so have its players. Wealth managers are shifting focus on providing comprehensive, multifaceted advice. Today, the easy accessibility of interactive tools enables customers to be more involved in the process and to experiment with the “what if” scenarios around basic planning.

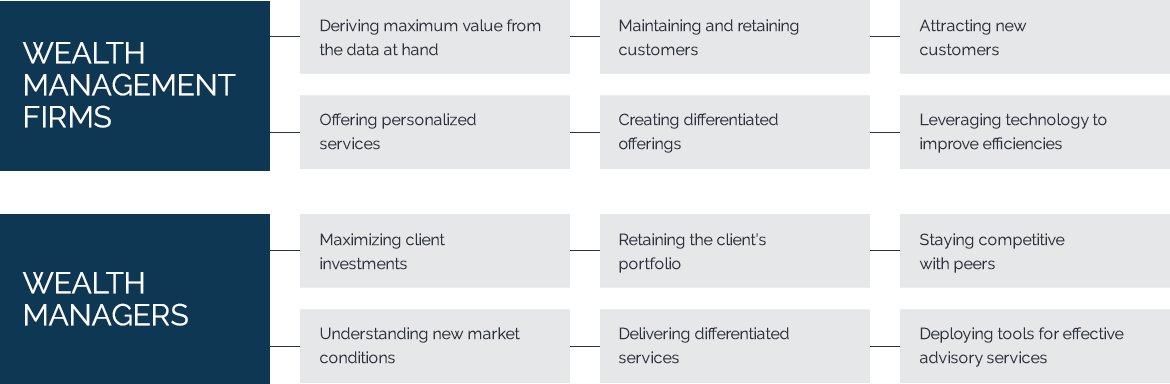

It is up to the wealth management firms and the individual wealth managers to stay relevant to their customer. As mentioned earlier, in the era of personalization and customization, one-size-fits-all models will not survive. The market span has widened beyond the traditional HNWI clients. In addition, emerging and disruptive technologies and new business models have created clear perspectives for the two sets of players in wealth management—the firms that provide wealth management services and the individual wealth managers that interact with customer daily. Figure 1 outlines the key priorities for both these parties. The key to success is to find the ways and means to converge these areas for success.

the two sets of players in wealth management—the firms that provide wealth management services and the individual wealth managers that interact with customers on a daily basis. Figure 1 outlines the key priorities for both these parties. The key to success is to find the ways and means to converge these areas for success.

EXCITING TIMES AHEAD FOR WEALTH MANAGERS

Whether it is reskilling your current wealth advisors or hiring digital talent externally, the future of the wealth management workforce is all about embracing technology as a trusted coworker and maximizing it to the client’s advantage.

Businesses are wholeheartedly embracing the opportunity to leverage these changes to improve business efficiencies, enhance revenues, and stay relevant to their customers. Increasing digitization and the proliferation of the Internet provides a broad spectrum of data sources and presently, two key drivers are currently shaping the evolution of successful financial planning and wealth management: data aggregation and data analytics. Leveraging the data, or rather big data, to create differentiated value for customers is an opportunity financial advisors cannot afford to miss.

There is no denying that the role of the financial advisor will change dramatically in the next few years. Not only will many customers expect better tools for engagement, but advisors will also likely be serving even more customers and for lower fees. They will need to deeply understand their clientele with the speed and precision of machine learning. With extraordinarily high volumes of managed assets at stake, advisors must be clear about what they need from their technology going forward.

Here are some interesting and exciting developments to look forward to in wealth management:

-

Data, data, and more data:

Data analytics and visualization tools are gaining popularity in extracting value from the existing data. Customers are not only looking to generate reports from data, but they also want the data to work more effectively for them. Making informed investments and business decisions with actionable, meaningful, and usable insights is critical. -

Robo-advisors:

While there is much debate about the quantity of assets currently being managed by robo- advisors, it’s still an innovation worth noticing. By 2020, an estimated USD1 trillion in total assets is expected to be managed by some form of robo-advisor or investment automation technology. Experts are casting aspersions in this regard because this level of automation inherently discredits the notions of customization and personalization in advisory services. -

The leading advisor:

After the global financial crisis, several firms had to tackle complex regulations coupled with trust issues from customers. In this scenario, individual advisors emerged as the stars. The focus is now on the experience, capabilities, and adaptability of the individual wealth manager or financial advisor to retain customers and sustain their confidence. -

An integrated approach to wealth management:

Investors have long been frustrated with the sheer number of firms, services, and advisors they must deal with to manage the various aspects of their financial health. People often have one firm they highly trust to manage their retirement investments, but need to go elsewhere to manage their housing or property-related assets. This needs to change. Wealth management firms that can offer this integrated approach stand a better chance at retaining long- term customers. -

Online is routine, mobile is catching up:

Mobile banking is catching up within the wealth management sector as well with secure and immediate access to investment accounts, balances, transactions and so much more. According to McKinsey, till about two years ago, 35 percent of customer interactions (compared with about 65 percent online) were on mobile and it is the fastest-growing channel across financial services.

CONCLUSION

The complexity with which businesses operate today can be simplified with the prudent use of data and analytics. The vast amount of data available today helps make accurate, agile, and effective decisions. For wealth managers, data is now a strategic asset and will continue to be so in future. With the rising demand for wealth managers, both wealth management firms and wealth managers can benefit tremendously from leveraging tools such as artificial intelligence, machine learning, and predictive as well as prescriptive analytics. For wealth management firms, it is not only about delivering better value to their customers, but also about managing wealth managers. Decoding the propensity and probability of an account to succeed, enhancing the clients’ aggregate information about their assets, comparing the performance of wealth managers, and focusing on the top performing wealth managers are only some of the advantages that can be leveraged with these new developments.

ABOUT THE AUTHOR

John Oberon is the President of DecisionMinesTM for Digital Excellence. His profound industry expertise helps orchestrate the DecisionMinesTM portfolio—from product management, development and support to business development, sales, and marketing.

John has decades of experience across the software industry. He has been a dexterous contributor to the technical innovation and agile development of leading organizations such as Cisco, Mashery, Intuit, and Microsoft.

John holds several patents, as well as a computer science degree from a California State University.

REFERENCES

- Investopedia – Wealth Management

- McKinsey (article) – Key trends in digital wealth management and what to do about them

- McKinsey (article) – How wealth managers can transform for the digital age